How to Get a Business Loan for Your Restaurant in 2026

📅 May 2026 · ⏱ 7 min read · Build&Fund Advisory Team

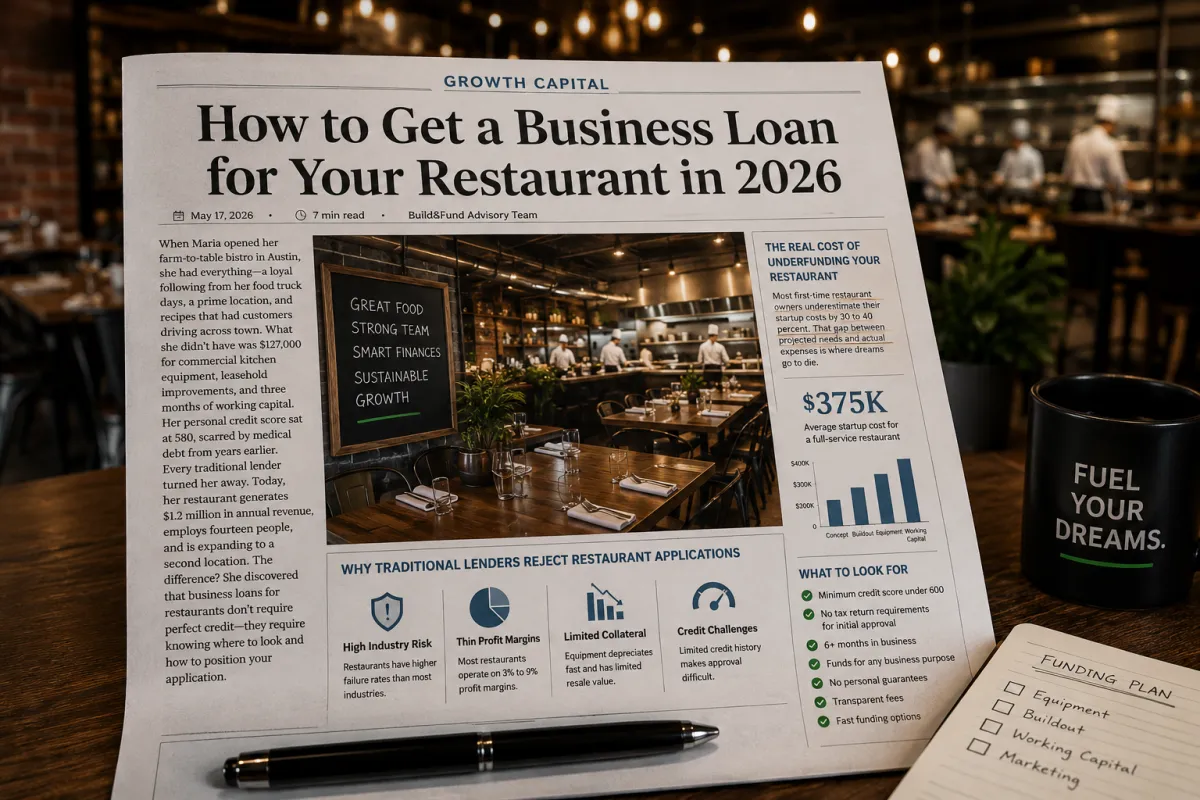

When Maria opened her farm-to-table bistro in Austin, she had everything—a loyal following from her food truck days, a prime location, and recipes that had customers driving across town. What she didn't have was $127,000 for commercial kitchen equipment, leasehold improvements, and three months of working capital. Her personal credit score sat at 580, scarred by medical debt from years earlier. Every traditional lender turned her away. Today, her restaurant generates $1.2 million in annual revenue, employs fourteen people, and is expanding to a second location. The difference? She discovered that business loans for restaurants don't require perfect credit—they require knowing where to look and how to position your application.

The Real Cost of Underfunding Your Restaurant

Restaurant ownership demands more capital than almost any other small business category. Between commercial-grade equipment, health department compliance, inventory that spoils, and payroll that can't wait, the cash demands never stop. Most first-time restaurant owners underestimate their startup costs by 30 to 40 percent, according to industry research. That gap between projected needs and actual expenses is where dreams go to die—not from bad food or poor service, but from running out of runway before the business hits its stride.

The consequences of underfunding extend far beyond the opening phase. Restaurants operating on thin margins often can't afford to fix equipment when it breaks, leading to menu limitations and customer disappointment. They can't stock up on ingredients when prices dip, missing opportunities to protect their margins. They can't hire enough staff to deliver consistent service, burning out their best employees. Each of these small compromises compounds until the business is fighting for survival rather than building toward growth.

Why Traditional Lenders Reject Restaurant Applications

Banks view restaurants as high-risk borrowers for reasons that have nothing to do with your specific business. Industry failure rates, while often exaggerated in popular culture, remain higher than most sectors. Profit margins typically run between 3 and 9 percent, leaving little cushion for loan repayment during slow periods. And the collateral restaurants offer—kitchen equipment, furniture, inventory—depreciates rapidly and has limited resale value. From a traditional lender's perspective, the numbers simply don't work for conventional underwriting.

Limited credit history compounds these structural challenges. If you've been operating primarily in cash, if your business is new, or if your personal credit took hits during economic downturns, you're facing a double barrier. Lenders see both industry risk and individual risk, and their algorithms aren't designed to recognize the factors that actually predict restaurant success: location quality, concept differentiation, operator experience, and community support. This disconnect between what banks measure and what matters leaves countless viable restaurants without access to growth capital.

Traditional bank rejection doesn't mean your restaurant isn't fundable—it means you're applying to the wrong funding sources for your current situation.

Step-by-Step: How to Secure Restaurant Funding With Limited Credit

- 1Assess Your True Funding Position

Before approaching any lender, gather your documentation and honestly evaluate where you stand. You need six months of bank statements, your current credit score, proof of time in business, and accurate revenue figures. Many restaurant owners discover their position is stronger than they assumed—annual revenue above $180,000 and a credit score above 500 qualifies you for multiple alternative lending programs. Understanding your numbers prevents wasted applications and helps you target appropriate funding sources.

- 2Explore SBA Loan Programs

The Small Business Administration backs loans up to $5 million for restaurants, with interest rates and fees capped by federal regulation. SBA 7(a) loans work for almost any business purpose—equipment, real estate, working capital, or debt refinancing. While approval takes longer than alternative options, the terms are significantly better. If your credit challenges are modest and you can wait several months for funding, SBA programs should be your first target. The government guarantee reduces lender risk, making approval possible even when conventional loans aren't.

- 3Consider Equipment Financing

Restaurant equipment loans use the equipment itself as collateral, reducing the lender's emphasis on your credit profile. If your primary need is kitchen equipment, refrigeration, or point-of-sale systems, equipment financing often offers faster approval and more flexible credit requirements than general business loans. The equipment secures the loan, which means lenders focus more on the value of what you're purchasing than on your personal financial history.

- 4Investigate Credit Stacking Strategies

Credit stacking involves strategically combining multiple funding sources—business credit cards, lines of credit, and term loans—to access larger amounts at better rates than any single source would offer. Done correctly, qualified business owners can access $50,000 to $250,000 at zero-percent introductory rates without personal guarantees. This approach requires understanding how to sequence applications and which products complement each other, but it can provide substantial funding even when traditional loans aren't available.

- 5Prepare a Compelling Business Case

Lenders who work with restaurants understand the industry differently than traditional banks. They want to see your concept's differentiation, your experience in food service, your location analysis, and your realistic financial projections. Prepare a concise document covering these elements—not a hundred-page business plan, but a focused explanation of why your specific restaurant will succeed. Include photos of your current operation, customer reviews, and any press coverage. Make it easy for the lender to say yes.

What to Look for in Restaurant Financing

- ✓ Minimum credit score requirements below 600

- ✓ No tax return requirements for initial approval

- ✓ Funding available for businesses with six months or more operating history

- ✓ Flexible use of funds including working capital, equipment, and renovations

- ✓ Transparent fee structures with no hidden prepayment penalties

- ✓ Funding timeline that matches your operational needs

- ✓ Options that don't require personal guarantees or home equity

Need Capital Without the Traditional Bank Runaround?

Our Business Funding and Credit Stacking Program helps restaurant owners access $50,000 to $250,000 at 0% introductory rates. No personal guarantee required for qualified applicants.

Learn More →Critical Mistakes Restaurant Owners Make When Seeking Funding

- Applying to too many lenders simultaneously. Multiple hard credit inquiries in a short period damage your score and signal desperation to lenders. Instead, research requirements thoroughly and apply strategically to your best-fit options first.

- Underestimating the amount needed. Requesting $50,000 when you actually need $80,000 means you'll be back seeking additional funding within months—often at worse terms because you've already taken on debt. Calculate your true needs, add a cushion for unexpected expenses, and request the full amount upfront.

- Ignoring the cost of capital in your projections. A loan with a 15% interest rate requires different pricing and margin management than one at 7%. Factor your financing costs into your business model before committing, ensuring the capital actually improves your position rather than creating an unsustainable payment burden.

Restaurant Funding Landscape: What the Data Shows

Understanding how different funding options compare helps you target your applications effectively. The restaurant financing market has expanded significantly in recent years, with alternative lenders filling gaps that traditional banks won't address. Approval rates, funding speeds, and typical amounts vary dramatically across loan types.

The difference between restaurants that survive their first five years and those that don't often comes down to one factor: access to the right capital at the right time. Business loans for restaurants exist across a spectrum from traditional SBA programs to innovative credit stacking approaches. Your job isn't to qualify for every option—it's to find the funding source that matches your current situation and growth objectives.

Limited credit history doesn't mean limited options. It means you need better information about where to apply and how to present your business. The restaurant industry's capital-intensive nature has spawned an entire ecosystem of lenders who understand food service economics and underwrite based on factors beyond personal credit scores. Your revenue trends, time in business, and operational stability matter more to these specialized funders than the credit mistakes of your past.

Discover Capital You Didn't Know You Could Access

Most restaurant owners leave money on the table—in unclaimed tax credits, inefficient payment processing, and overlooked funding options. Our free analysis identifies exactly where your hidden revenue is waiting.

Get Your Free Hidden Revenue Analysis →Or explore our Business Funding and Credit Stacking Program