Reduce Processing Fees Restaurant Owners Pay in 2026

📅 May 2026 · ⏱ 7 min read · Build&Fund Advisory Team

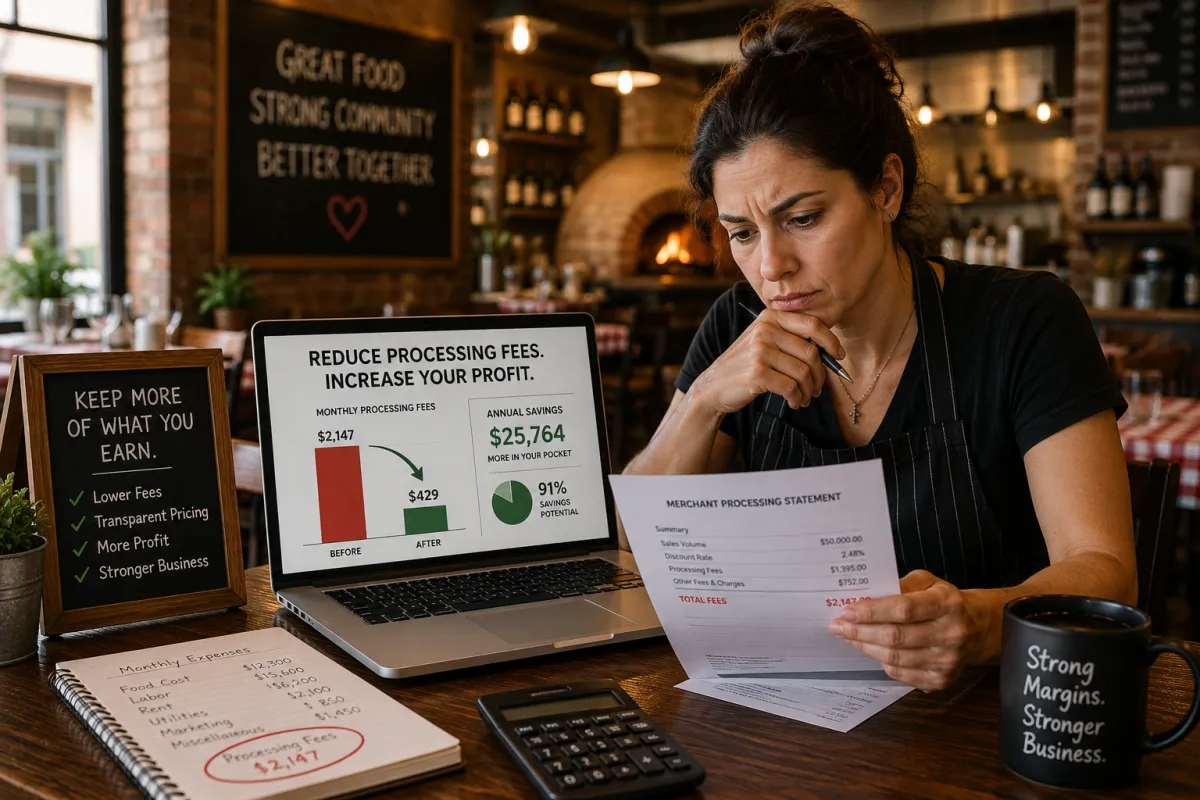

Maria runs a family-owned Italian restaurant in Phoenix. Her red sauce recipe came from her grandmother. Her work ethic came from decades of sixteen-hour days. But when her accountant sat her down last quarter, the numbers told a story no family recipe could fix: $2,147 per month—vanishing into credit card processing fees. That's $25,764 a year. Enough to hire another line cook. Enough to finally upgrade the aging walk-in cooler. Instead, it evaporates before Maria ever sees it. If you're searching for ways to reduce processing fees restaurant owners face daily, you're not alone—and you're not powerless.

The Real Cost of Credit Card Processing for Restaurants

The restaurant industry operates on margins so thin they'd make other business owners weep. While the average American business enjoys profit margins between fifteen and twenty percent, restaurants typically scrape by on three to nine percent. Every dollar matters. Every unnecessary expense threatens survival. Yet most restaurant owners treat processing fees as an unchangeable line item—fixed, inevitable, untouchable. This assumption costs them dearly.

The average small business pays between 1.5% and 3.5% of every single transaction just to process credit and debit cards. For a restaurant doing $50,000 per month in card sales, that translates to $750 to $1,750 disappearing every thirty days. Over a year, you're looking at $9,000 to $21,000—money that never touches your operating account, never funds your next equipment upgrade, never becomes a performance bonus for your best server. The payment processors know you're too busy running a restaurant to scrutinize their statements. They count on it.

Why Payment Processors Get Away With This

The payment processing industry thrives on complexity by design. Your monthly statement arrives packed with line items that seem intentionally confusing: interchange fees, assessment fees, PCI compliance charges, batch fees, statement fees, and mysterious "miscellaneous" charges that no one at customer service can adequately explain. This opacity isn't accidental. When you can't understand what you're paying for, you can't negotiate it down. When the fees spread across dozens of cryptic categories, the true total stays hidden until someone like your accountant adds it all up and delivers the bad news.

Restaurant owners face additional vulnerability because of how card transactions flow through their businesses. Tips complicate the math. Split checks multiply the fees. High transaction volumes with moderate ticket sizes mean you're paying that percentage cut hundreds of times per day. Meanwhile, junk fees pile on: PCI non-compliance penalties for paperwork you didn't know existed, equipment rental charges for terminals you thought you owned, early termination threats that lock you into unfavorable contracts. The processors designed this system. They benefit when you stay confused.

Payment processors profit from confusion. The more complex your statement, the harder it becomes to identify unnecessary charges—and the more money quietly leaves your business every month.

How to Reduce Processing Fees at Your Restaurant: A Step-by-Step Approach

- 1Audit Your Current Processing Statements

Before you can fix the problem, you need to understand it. Gather your last six months of processing statements and calculate the total fees paid—not just the headline rate, but every charge on every page. Divide the total fees by your total card sales volume to find your effective rate. Many restaurant owners discover their "2.5% rate" actually works out to 3.4% or higher once all the hidden charges get included. This number is your baseline. Everything else you do aims to lower it.

- 2Understand Dual Pricing and Cash Discount Programs

Zero-fee processing isn't magic—it's a pricing structure. With dual pricing, you present two prices: a cash price and a card price that includes the cost of acceptance. Done correctly, with clear signage, proper receipt language, and correctly configured POS settings, this approach eliminates your processing costs without hurting guest satisfaction. Customers choose their preferred payment method with full transparency. You stop subsidizing the credit card companies' rewards programs out of your razor-thin margins.

- 3Negotiate or Renegotiate Your Processing Agreement

Most restaurant owners sign their initial processing contract and never revisit it. That's a mistake. Your transaction volume gives you leverage. If you're processing $40,000 or more monthly, you have room to negotiate better interchange-plus pricing, reduced monthly fees, or elimination of junk charges. Even if you don't switch providers, the threat of leaving often produces sudden "loyalty discounts" your current processor never mentioned before.

- 4Eliminate Hidden Junk Fees

Comb through your statements for charges that provide no value: PCI non-compliance fees (often fixable by completing a simple online questionnaire), statement fees (request electronic statements), batch fees charged at excessive rates, and vague "service" charges with no clear explanation. These nickle-and-dime items can add $50 to $200 monthly—$600 to $2,400 annually—without delivering any benefit to your operation.

- 5Upgrade or Optimize Your POS System

Your point-of-sale system affects your processing costs more than you might realize. Outdated terminals that don't support chip or contactless payments often trigger higher interchange rates. Systems that don't properly settle batches daily cost you money. POS platforms with built-in processing often charge premium rates because switching feels too complicated. Evaluate whether your current setup serves your financial interests or your processor's.

What to Look for in a Processing Partner

- ✓ Transparent interchange-plus pricing with no bundled rate obscuring the true cost

- ✓ Month-to-month contracts with no early termination fees or equipment lease traps

- ✓ Clear support for dual pricing or cash discount programs if you choose to implement them

- ✓ Statements you can actually understand, with every fee explained and justified

- ✓ No PCI non-compliance fees, monthly minimums, or mysterious service charges

- ✓ Free equipment or reasonable purchase options—never long-term leases at inflated prices

- ✓ Responsive customer support that answers questions without transferring you five times

Stop Paying Thousands in Processing Fees Every Month

Build&Fund's Cash Discount Merchant Processing program helps restaurant owners eliminate credit card processing fees entirely through compliant dual pricing. Keep the money you've been handing to processors—without changing how your customers pay.

Learn More →Common Mistakes Restaurant Owners Make With Processing Fees

- Accepting the first rate offered without negotiation. Processors expect pushback. When you don't negotiate, they keep margins high. Always ask for better interchange-plus rates, especially if you've been a customer for over a year or process significant volume.

- Ignoring statements because they're confusing. That confusion is intentional. Set a calendar reminder to review your processing statement every month. Look for new fees, rate increases, or charges that don't match your understanding of the agreement. What you don't catch, you keep paying.

- Fearing customer pushback on cash discount programs. Modern consumers understand that card acceptance costs businesses money. With proper signage explaining that the listed price is the cash price and card payments include a small service fee, most customers either pay with cash, accept the card price without complaint, or don't notice at all. The restaurants that implement dual pricing properly report minimal customer friction and significant cost savings.

Processing Fees Impact Across Restaurant Types

The burden of payment processing doesn't fall equally across all restaurant concepts. Quick-service restaurants with high transaction counts and low average tickets often suffer most—paying that percentage fee on hundreds of $12 and $15 transactions adds up fast. Full-service establishments may see larger individual tickets, but their volume still generates substantial monthly fees. Understanding where your restaurant falls helps you prioritize the right cost-reduction strategies.

These figures assume typical processing rates for each segment. Your actual costs depend on your specific agreement, but the pattern holds: higher transaction counts and lower average tickets mean higher effective rates and more total fees. Restaurants processing $50,000 monthly in cards commonly lose $17,000 to $24,000 annually—enough to fund equipment upgrades, additional staff, marketing campaigns, or simply provide a cushion against the next unexpected expense.

Taking Back Control of Your Restaurant's Margins

Every swipe, tap, and chip insertion quietly transfers money from your register to processors who bank on your inattention. But you didn't build your restaurant to subsidize credit card companies. You built it to serve your community, support your family, and create something lasting. The strategies outlined above—auditing your statements, understanding dual pricing, eliminating junk fees, and choosing transparent processing partners—give you a path to reduce processing fees restaurant owners too often accept as unchangeable.

The restaurant industry enters each year ready to prove its resilience. Rising costs, tight margins, and economic uncertainty demand owners find every possible efficiency. Payment processing represents one of the largest controllable expenses in your operation. The question isn't whether you can afford to address it. The question is whether you can afford not to.

Discover How Much Revenue You're Losing to Hidden Fees

Most restaurant owners underestimate what processing fees actually cost them. Our free Hidden Revenue Analysis identifies exactly where your money goes—and how to get more of it back.

Get Your Free Hidden Revenue Analysis →Or explore our Cash Discount Merchant Processing