How to Eliminate Credit Card Processing Fees in 2026

📅 April 2026 · ⏱ 7 min read · Build&Fund Advisory Team

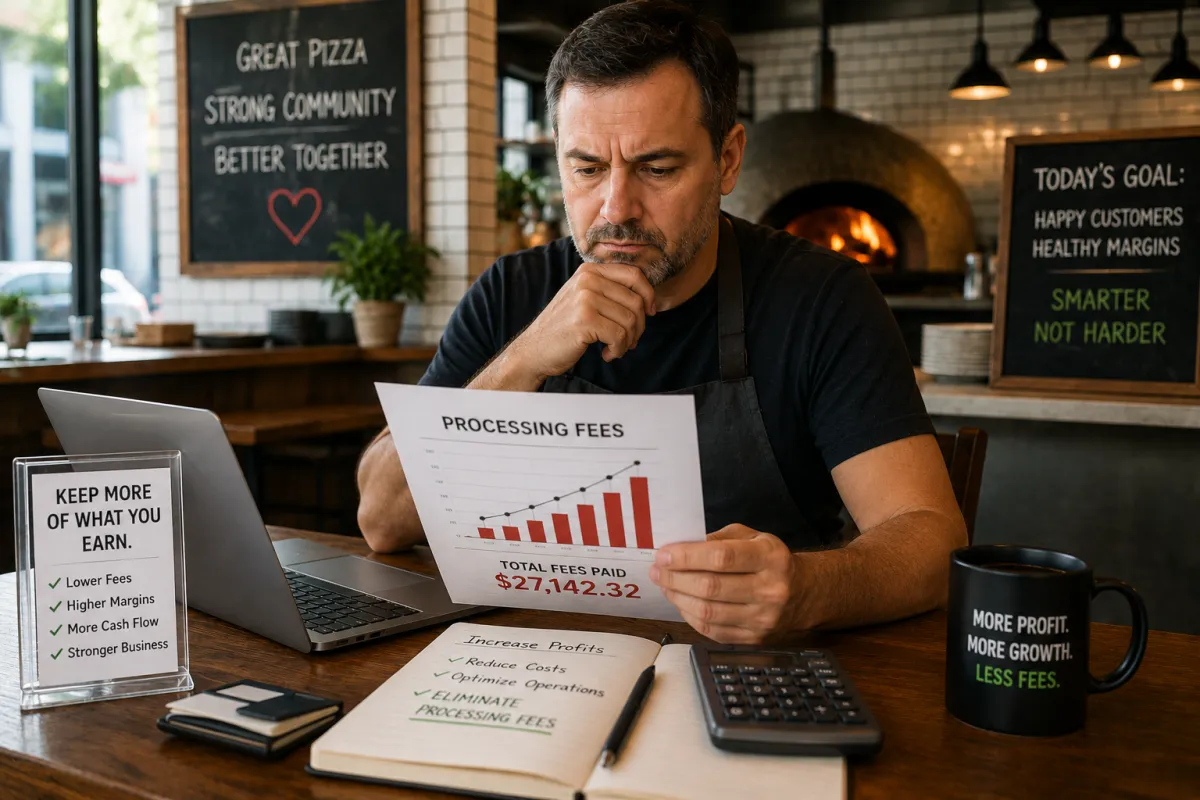

A family-owned pizzeria in Chicago recently discovered something alarming during a quarterly review: they had paid more than $27,000 in credit card processing fees over the past year. That figure exceeded what they spent on utilities, insurance, and marketing combined. The owner, who had operated the restaurant for fifteen years, had simply accepted these fees as an unavoidable cost of doing business. But here's the truth that transformed his bottom line—and can transform yours: learning how to eliminate credit card processing fees is not only possible, it's becoming standard practice for savvy small business owners across the country.

The Real Cost of Credit Card Processing Fees

Every swipe, tap, or online checkout quietly siphons between 2% and 4% of your hard-earned revenue straight into the pockets of payment processors. For a retail boutique processing $30,000 monthly in card transactions, that translates to $600 to $1,200 vanishing before you ever see it. Scale that up to a busy restaurant doing $50,000 per month, and you're hemorrhaging $1,500 to $2,000 monthly—money that could fund new equipment, staff bonuses, or expansion plans.

What makes this particularly painful is the compounding effect over time. These aren't one-time expenses; they're perpetual drains that grow alongside your success. The more your business thrives, the more you pay. A service business that doubles its revenue doesn't just double its processing fees—it often sees those fees increase disproportionately as transaction volumes trigger different rate tiers and additional per-transaction charges stack up.

Why Small Businesses Keep Paying These Fees

The credit card processing industry has spent decades conditioning merchants to believe that swipe fees are simply the price of admission to modern commerce. Processors rarely volunteer information about alternatives, and the complexity of interchange rates, assessment fees, and markup structures keeps most business owners confused enough to accept whatever terms they're offered. Many entrepreneurs sign merchant agreements without fully understanding the tiered pricing models or the hidden fees buried in pages of fine print.

Additionally, there's a widespread misconception that passing processing costs to customers will drive them away. This fear keeps countless business owners trapped in an expensive status quo. Yet consumer behavior data tells a different story: when given transparency about payment costs and options, most customers understand and accept the reality that card payments carry costs. The businesses that have made the shift report minimal customer pushback and significant profit recovery.

The average small business owner has never been shown compliant alternatives to absorbing processing fees—not because those alternatives don't exist, but because processors profit from merchant confusion.

How to Eliminate Credit Card Processing Fees: A Step-by-Step Approach

- 1Audit Your Current Processing Costs

Before making any changes, you need complete visibility into what you're actually paying. Request a full statement analysis covering at least three months of transactions. Look beyond the advertised rate to identify interchange markups, batch fees, PCI compliance charges, statement fees, and any other line items eating into your margins. Many business owners are shocked to discover their effective rate is significantly higher than the rate they were quoted.

- 2Understand Cash Discount Programs

A cash discount program allows you to post your prices at the card rate and offer a discount to customers who pay with cash or debit. This approach is legally compliant in all fifty states and follows card network rules when implemented correctly. Unlike surcharging, cash discounting focuses on rewarding cash payers rather than penalizing card users—a subtle but important distinction that affects both compliance and customer perception.

- 3Evaluate Surcharging as an Alternative

Credit card surcharging—adding a fee at checkout for customers who pay by credit card—is now permitted in most states, though specific rules vary. Surcharges cannot exceed your actual processing costs or 3%, whichever is lower. Proper signage and disclosure are mandatory. If your state permits surcharging and your customer base skews toward credit card users, this model may recover more fees than cash discounting alone.

- 4Upgrade Your Point-of-Sale System

Legacy POS systems often lack the functionality to implement compliant fee recovery programs. Modern terminals and software can automatically calculate discounts or surcharges, print required disclosures on receipts, and ensure every transaction meets card network requirements. The right technology makes the transition seamless for both you and your customers.

- 5Partner with a Compliant Processing Provider

Not all merchant services providers support fee elimination programs, and fewer still implement them correctly. You need a partner who understands the regulatory landscape, provides compliant signage and receipt configurations, and offers transparent pricing without hidden markups. The wrong provider can expose you to card network violations and customer complaints.

- 6Train Your Staff and Communicate with Customers

Transparency is essential for a smooth transition. Train your team to explain the program positively—emphasizing the cash discount rather than framing card payments as penalized. Update your signage at entry points and checkout areas. Most customers appreciate honesty about business costs, especially when they have the option to save money themselves.

What to Look for in a Fee Elimination Program

- ✓ Full compliance with Visa, Mastercard, and Discover network rules

- ✓ State-by-state regulatory compliance verification

- ✓ Transparent, flat-rate pricing with no hidden fees

- ✓ Automated discount or surcharge calculation at the terminal

- ✓ Compliant signage and receipt language provided

- ✓ Modern POS hardware that supports dual pricing

- ✓ Dedicated support for implementation and ongoing questions

- ✓ No long-term contracts or early termination penalties

- ✓ Clear reporting showing fees recovered each month

Stop Giving Away Thousands Every Month

Build&Fund's Cash Discount Merchant Processing program helps small businesses legally eliminate credit card processing fees while staying fully compliant with card network rules. See how much you could recover starting this month.

Learn More →Common Mistakes When Trying to Reduce Processing Costs

- Implementing non-compliant surcharges: Some business owners attempt DIY surcharging without understanding card network rules, resulting in violations that can lead to fines or termination of their merchant account. Surcharges that exceed actual costs, fail to provide proper disclosure, or apply to debit card transactions are all compliance landmines.

- Focusing only on the quoted rate: A processor advertising a low rate often makes up the difference through interchange-plus markups, monthly fees, and junk charges. Evaluating offers based solely on the headline rate leads many businesses into contracts that cost more than their previous arrangements.

- Neglecting staff training: Even the best fee elimination program fails when frontline employees can't explain it to customers. Confusion at checkout creates friction, generates complaints, and can undermine the entire initiative. Invest time in preparing your team before launch.

Where Your Processing Fees Actually Go

Understanding the breakdown of credit card processing costs helps illustrate why these fees are so difficult to negotiate down—and why passing them to the card-paying customer makes economic sense. The largest portion goes directly to the card-issuing banks as interchange, a fee that merchants have virtually no power to influence. The remaining portions flow to card networks and your payment processor.

As this breakdown shows, roughly 70% of what you pay never even reaches your processor—it goes to the banks that issued your customers' cards. This explains why negotiating with your processor yields limited results: they control only a fraction of the total cost. The only way to truly eliminate these fees is to shift them away from your business entirely through compliant cash discount or surcharge programs.

The path to eliminating credit card processing fees isn't complicated, but it does require the right strategy and the right partner. Whether your business processes $10,000 or $100,000 monthly in card transactions, the same principles apply: understand what you're paying, implement a compliant program, and recover revenue that rightfully belongs on your bottom line. Thousands of small businesses have already made this shift, redirecting tens of thousands of dollars annually from processors back into their operations. The only question is how much longer you'll wait before joining them.

Find Out How Much Revenue You're Leaving on the Table

Most small business owners are stunned to see their true processing costs calculated. Our free Hidden Revenue Analysis shows you exactly what you're paying and how much you could recover.

Get Your Free Hidden Revenue Analysis →Or explore our Cash Discount Merchant Processing